Search for topics or resources

Enter your search below and hit enter or click the search icon.

In today's ever-evolving global landscape, the ability to make fast, easy, and confident decisions is key to building a productive and enjoyable employee experience.

As the demands of the modern workforce continue to increase, so does the need for accurate and actionable data to make important decisions. Recognizing this need, the Occupancy Intelligence Index provides an unparalleled collection of occupancy data and benchmarks captured from VergeSense data, the largest and most accurate dataset on the market.

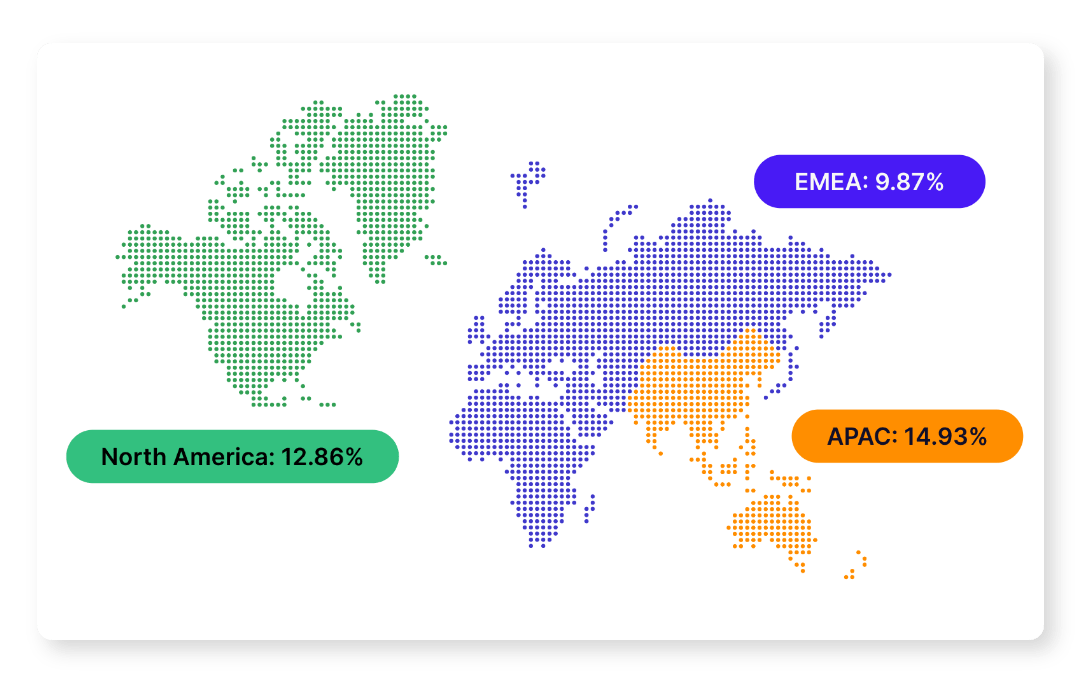

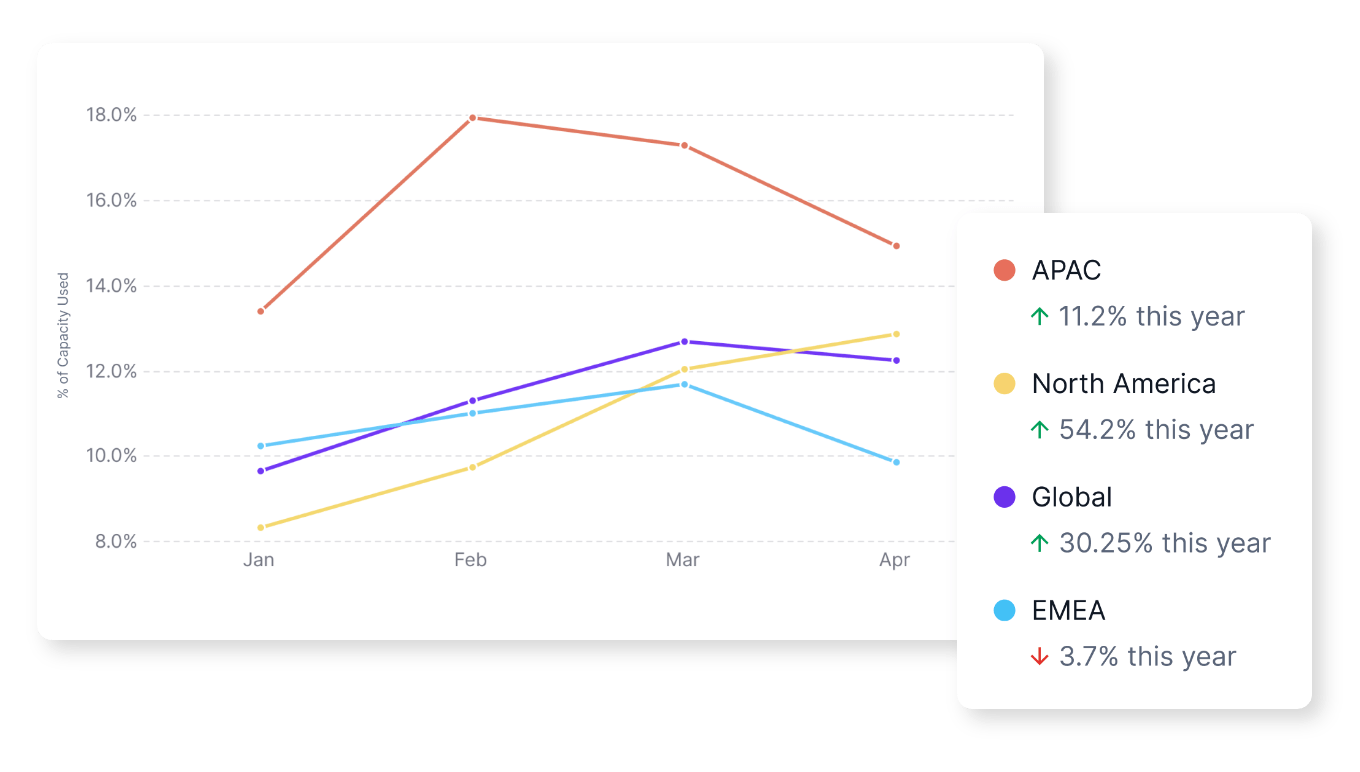

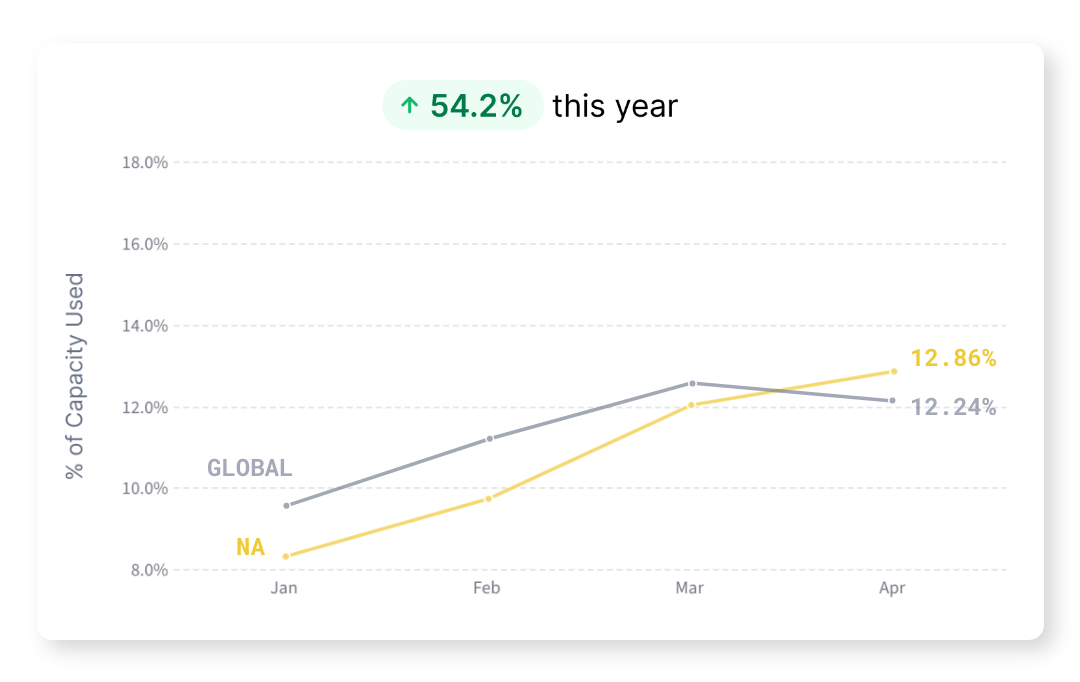

Globally, capacity usage continues to rise. The EMEA region, however, has not shown significant growth so far this year. Conversely, the APAC and North American regions have continued to experience steady usage growth.

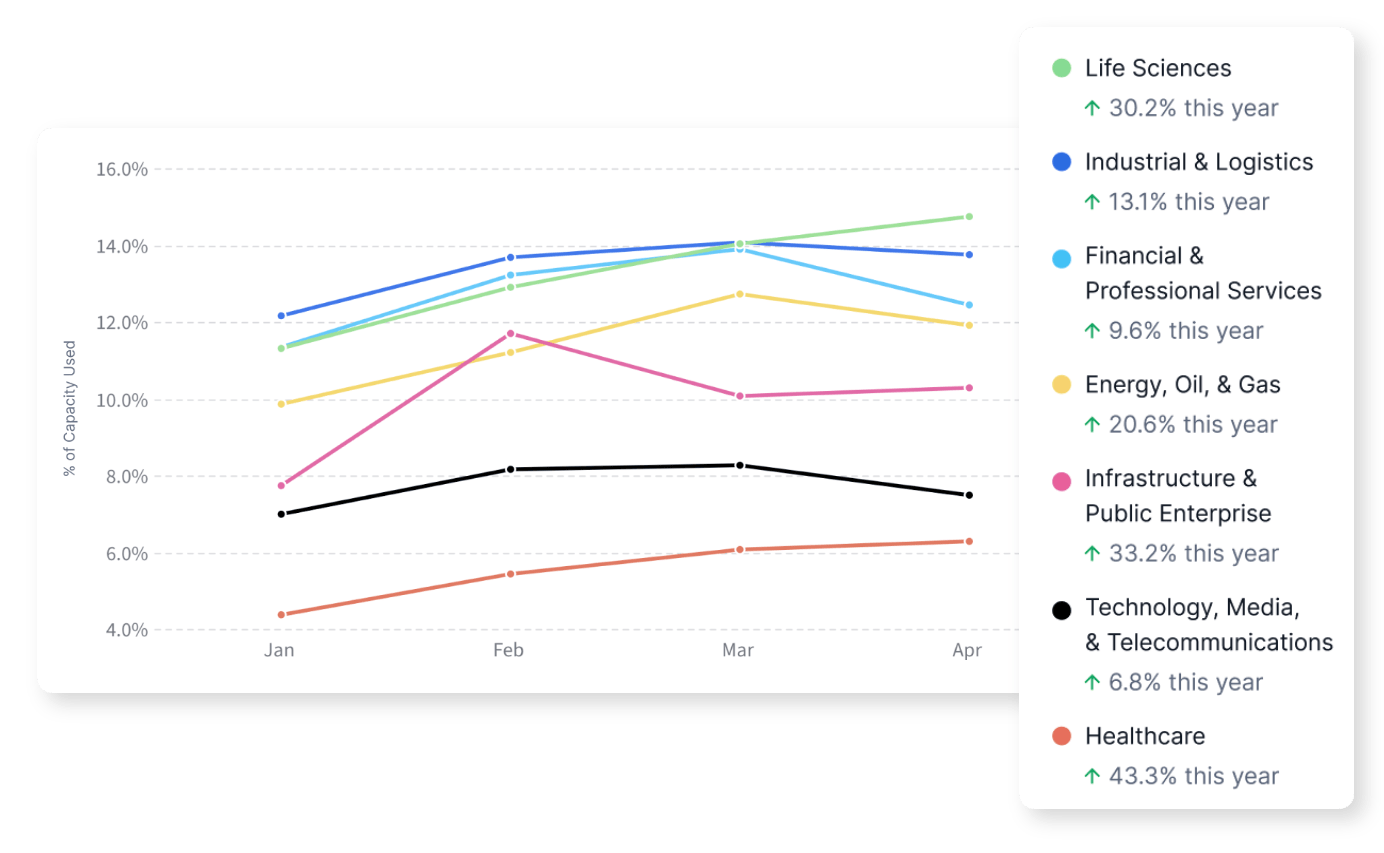

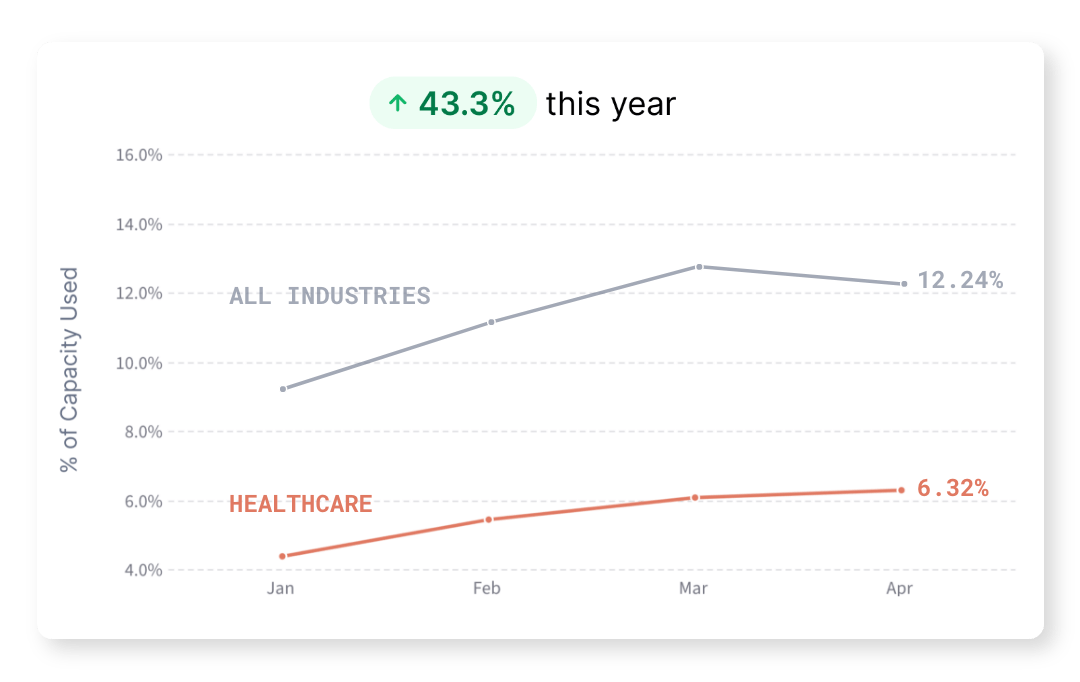

Capacity usage across all industries has been steadily increasing as well, with the rate of growth appearing to be correlated to the prevalence of return-to-office mandates and the necessity of in-office work for certain job functions within the verticals.

Even with RTO mandates and a steady increase in capacity usage, it's clear that most organizations across the globe still have ample room to increase office utilization. As a result, workplace leaders must make high-quality optimization decisions to increase space usage, boost productivity, and foster collaboration.

The Occupancy Intelligence Index utilizes four key terms to give insight into occupancy: capacity and space usage, focus spaces, and collaborative spaces.

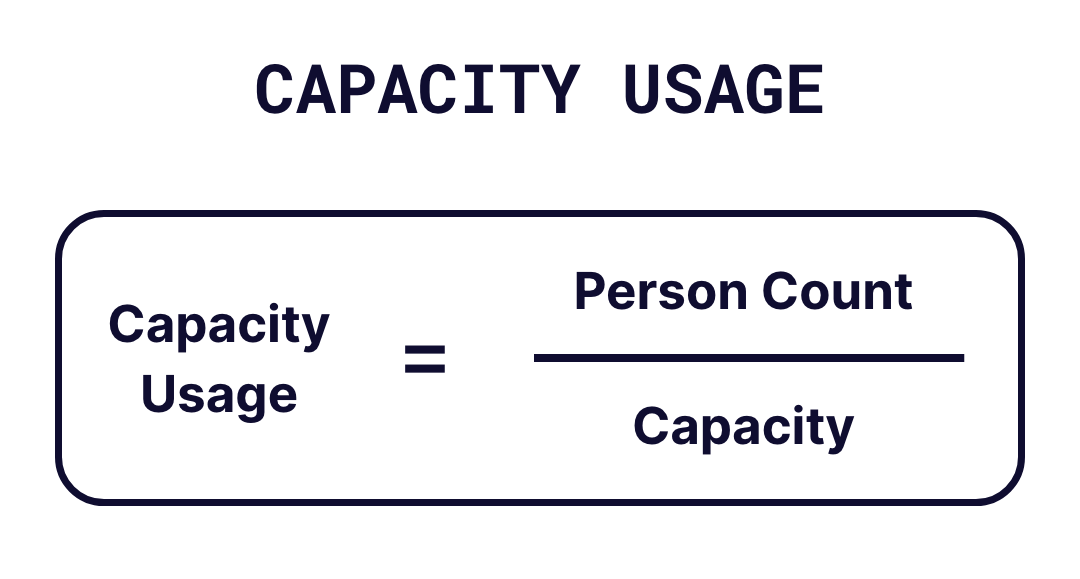

Capacity usage highlights how much of your workplace is being used by dividing the capacity of a building or space by how many people are using it.

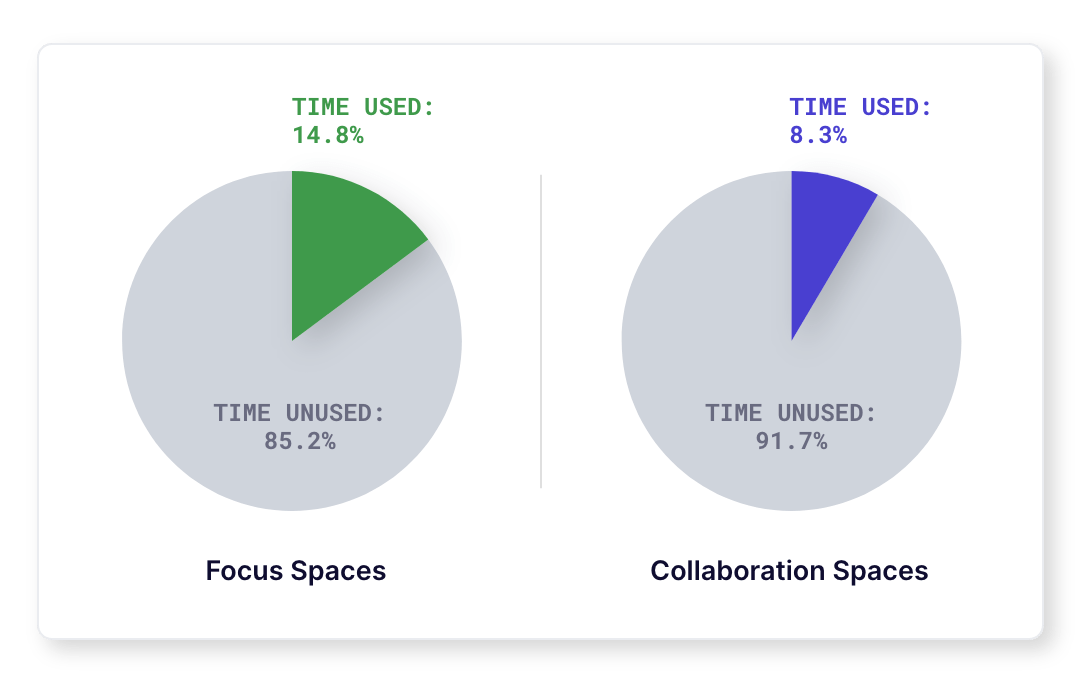

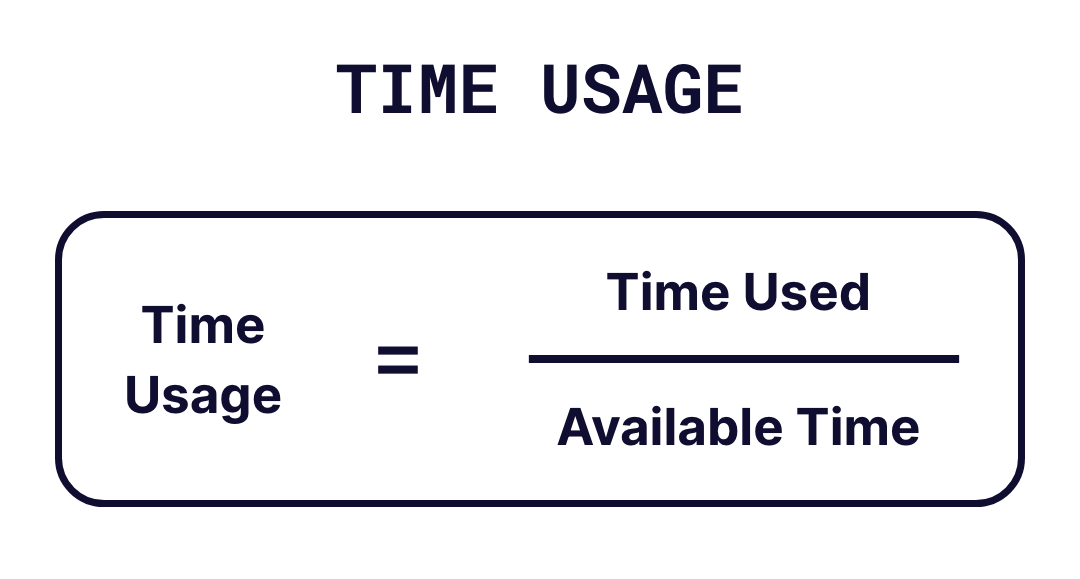

Time usage provides insight into the frequency and duration of space use. It is calculated by dividing the total time the measured spaces were in use by the total working hours.

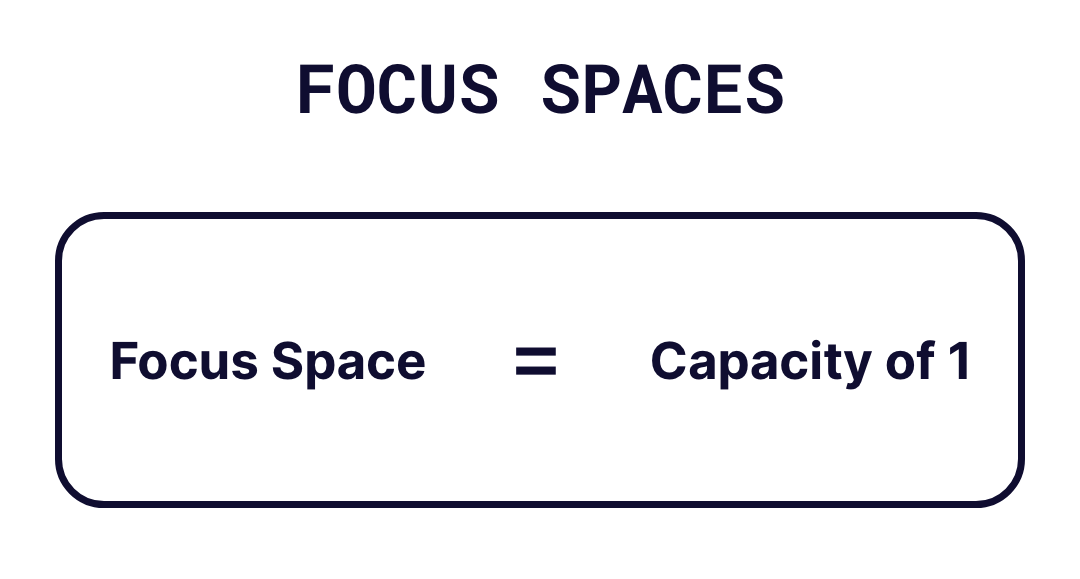

Focus spaces are those that have a capacity of one and are designed for individual work, such as a desk, phone booth, 1-person offices, etc.

Collaboration spaces are those that have a capacity greater than one and are designed for multiple people to utilize simultaneously, like conference rooms, whiteboarding spaces, huddle rooms, etc.

See first-hand the powerful dashboards, data, and insights you can leverage for your workplace decisions.

.jpg?width=1080&height=943&name=Talk-to-specialist-min%20(1).jpg)

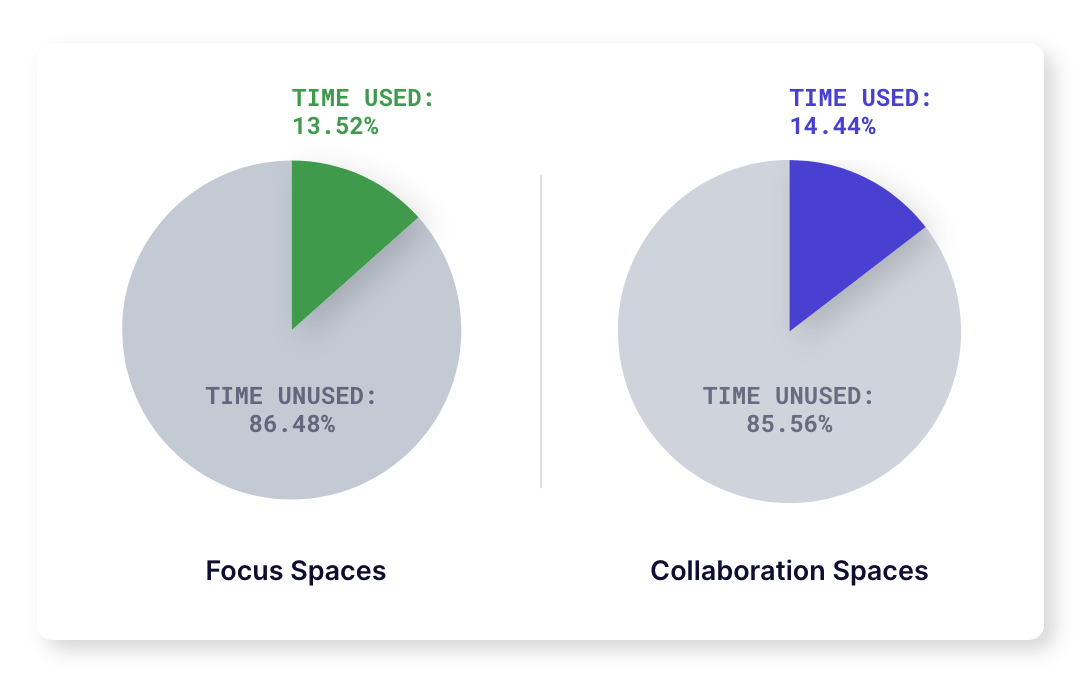

Overall, the global state of occupancy is increasing from a combined impact of return-to-office mandates, fewer remote job postings, and regional efforts to boost in-office collaboration. Globally, there was a small dip in capacity usage in April, likely influenced by public holidays and employees taking time off as the northern hemisphere nears summertime.

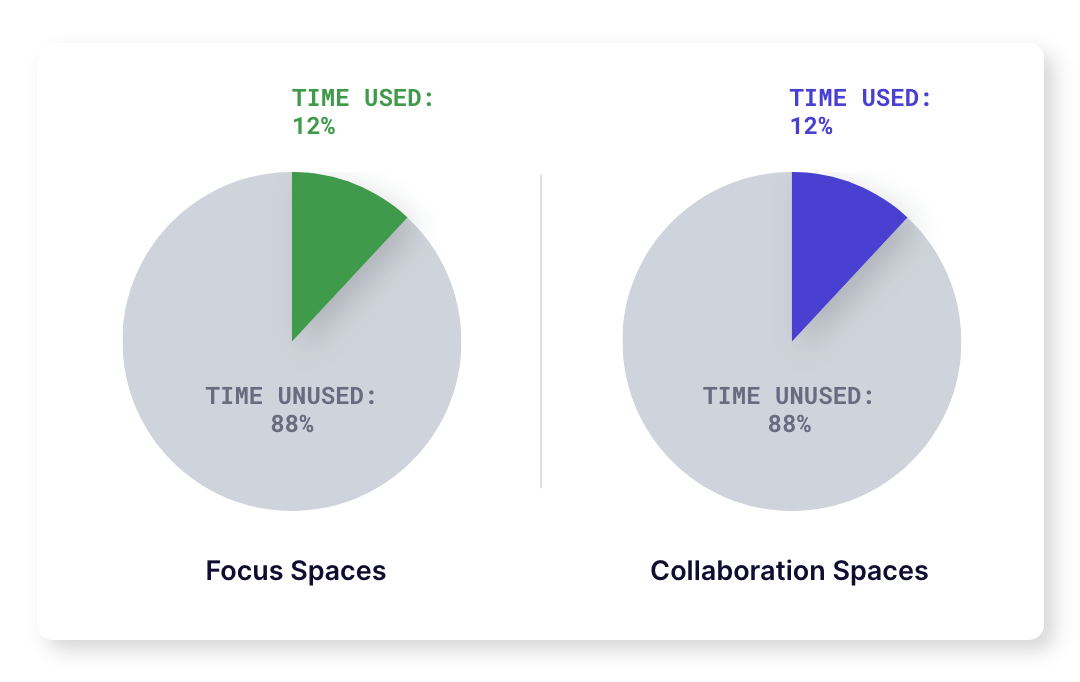

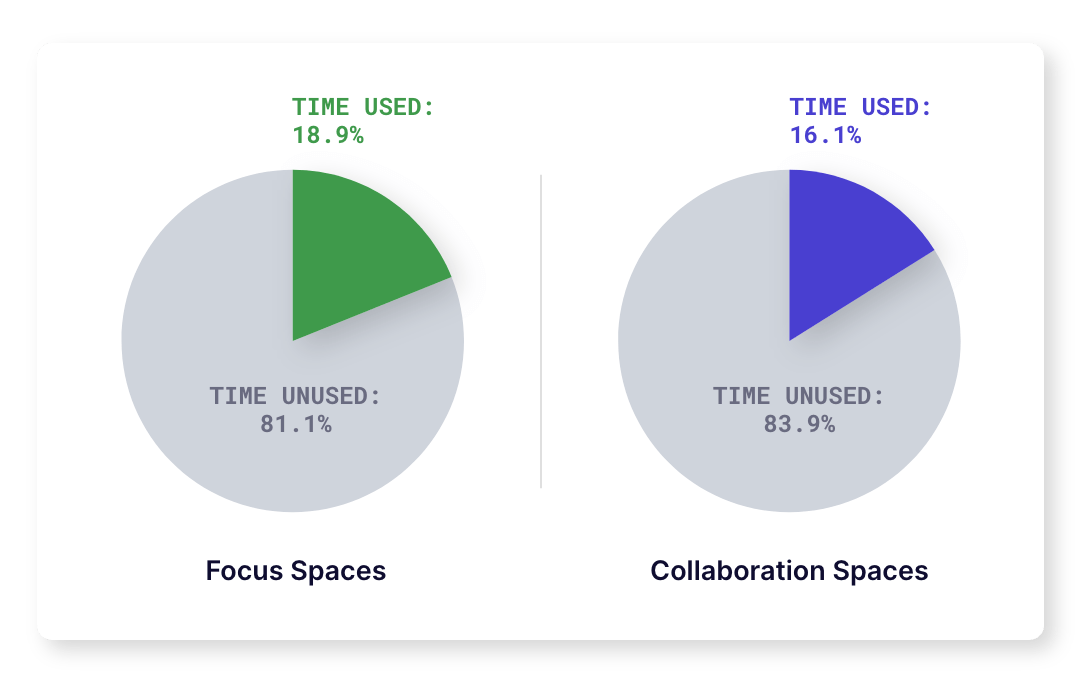

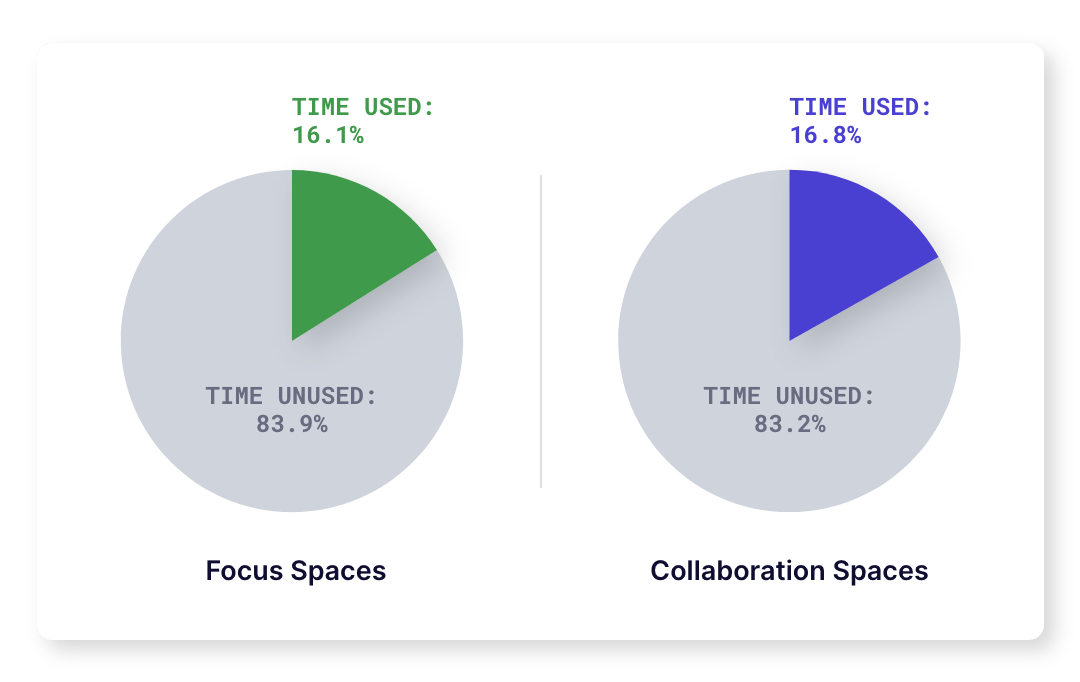

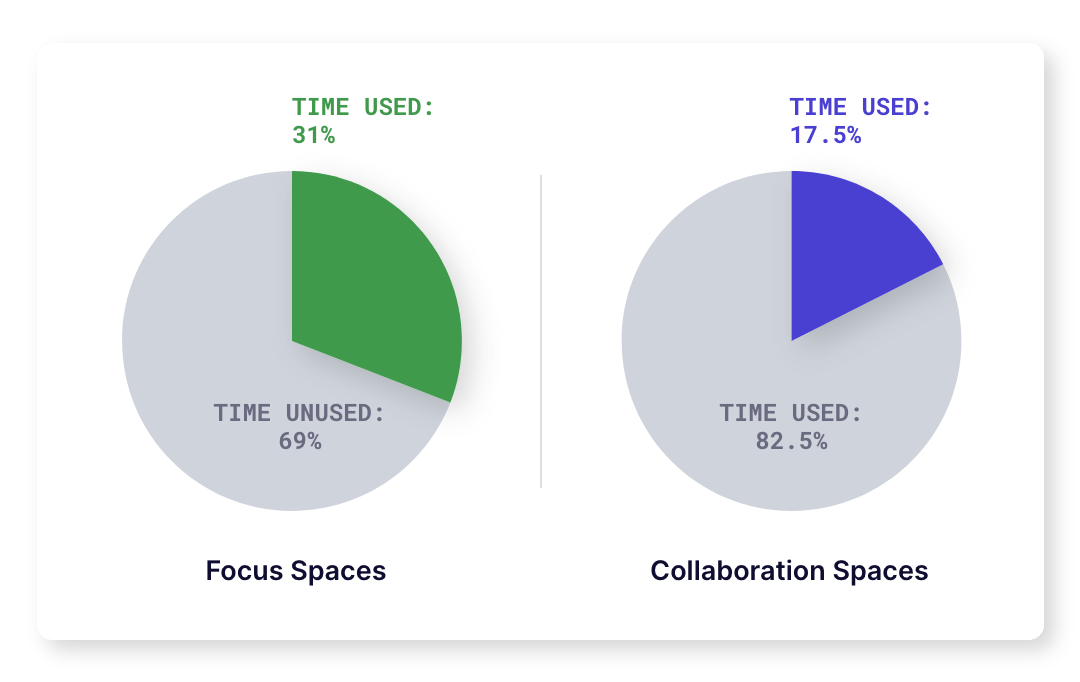

Overall, the global state of occupancy is increasing from a combined impact of return-to-office mandates, fewer remote job postings, and regional efforts to boost in-office collaboration. Globally, there was a small dip in capacity usage in April, likely influenced by public holidays and employees taking time off as the northern hemisphere nears summertime. Globally, collaboration spaces are being used a bit more frequently than focus spaces, showing that employees are utilizing in-person workdays as opportunities to collaborate with their teammates rather than just working heads-down or attending virtual meetings.

Globally, collaboration spaces are being used a bit more frequently than focus spaces, showing that employees are utilizing in-person workdays as opportunities to collaborate with their teammates rather than just working heads-down or attending virtual meetings.

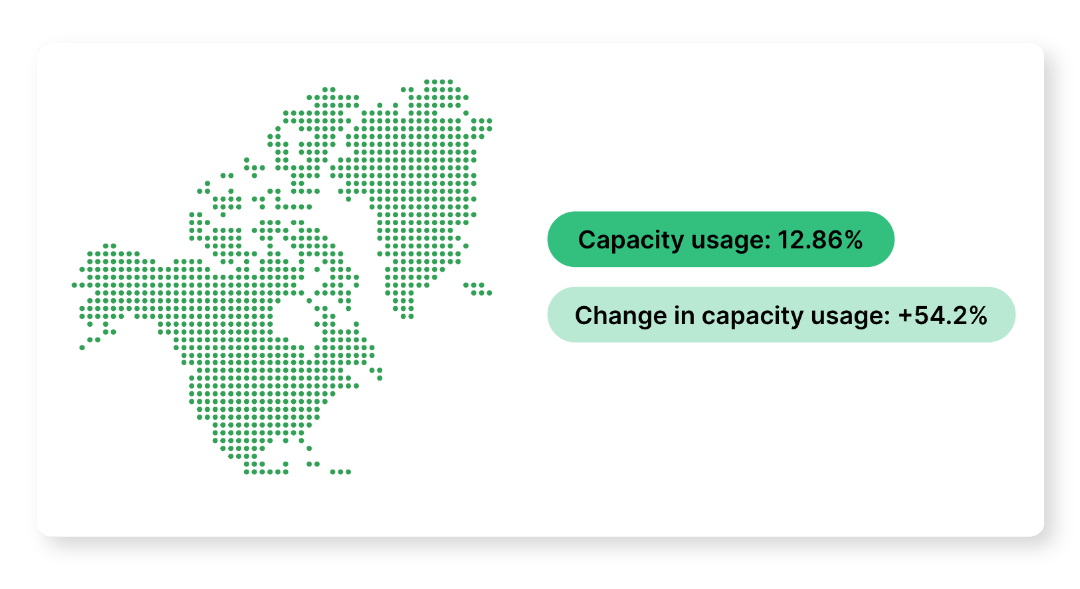

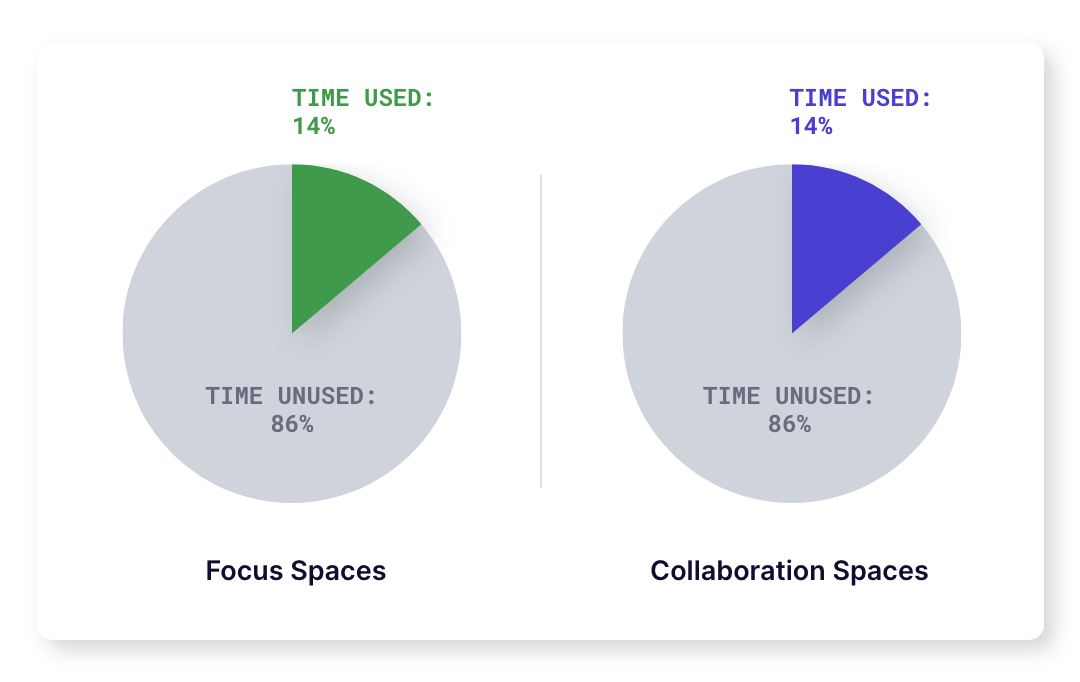

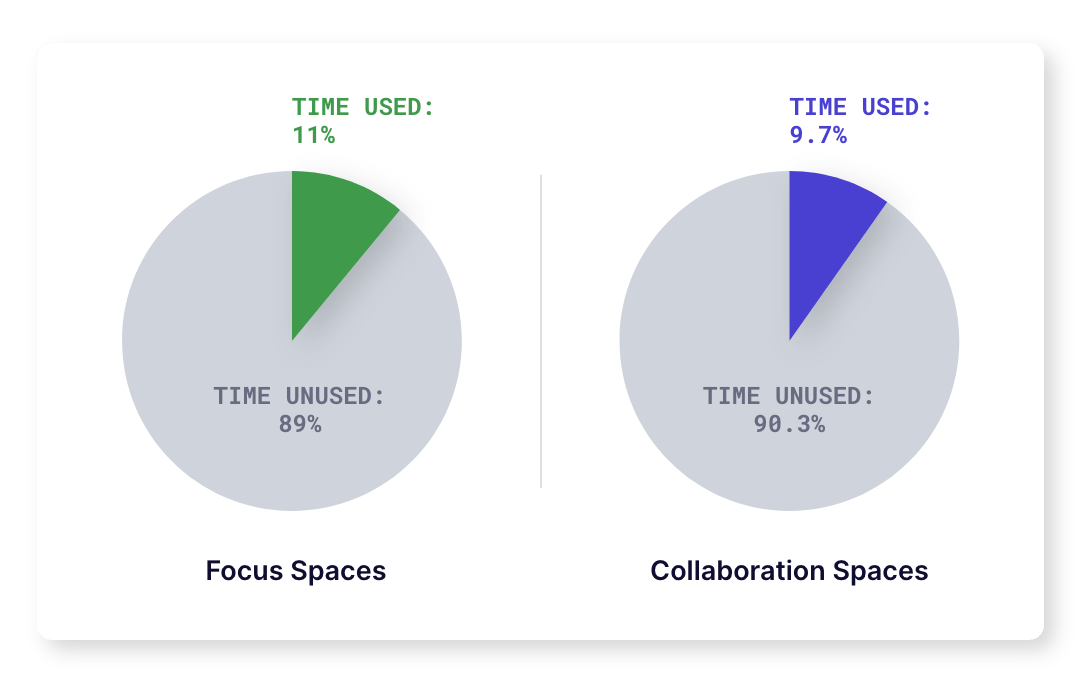

North America shows lower usage of collaborative spaces compared to other regions. All regions, but especially North America, have faced the challenge of their employees continuing to attend virtual meetings when working in-office, which could also be driving down the use of collaborative spaces.

North America shows lower usage of collaborative spaces compared to other regions. All regions, but especially North America, have faced the challenge of their employees continuing to attend virtual meetings when working in-office, which could also be driving down the use of collaborative spaces.

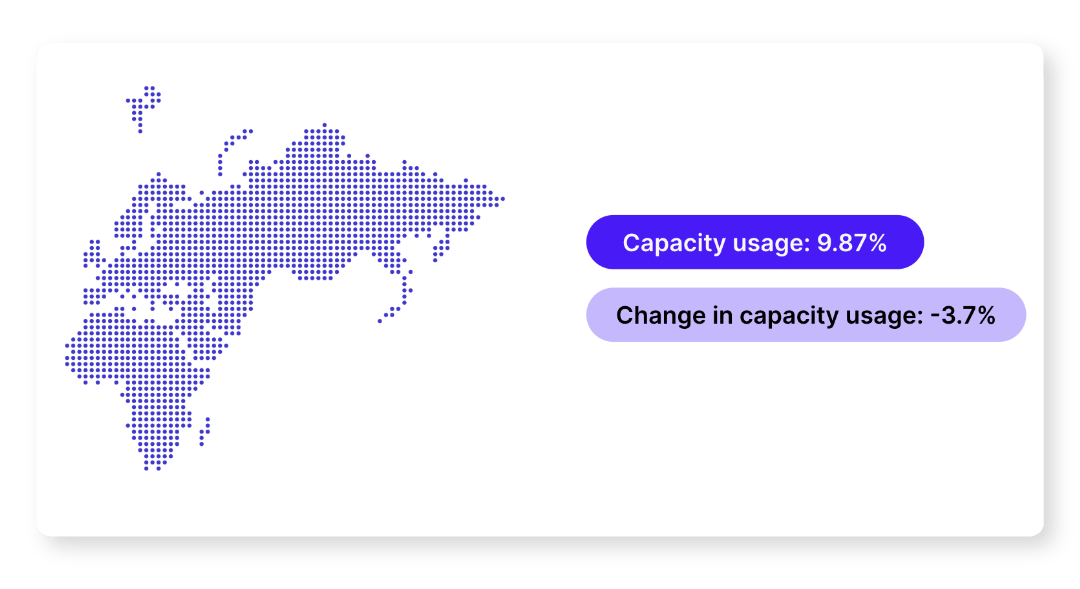

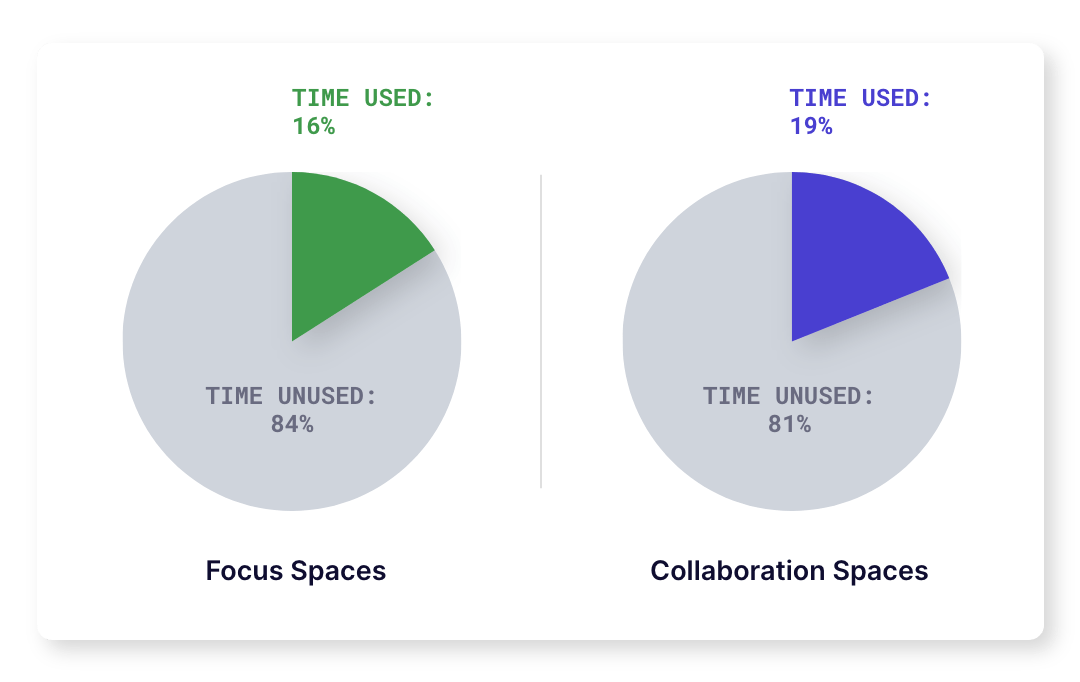

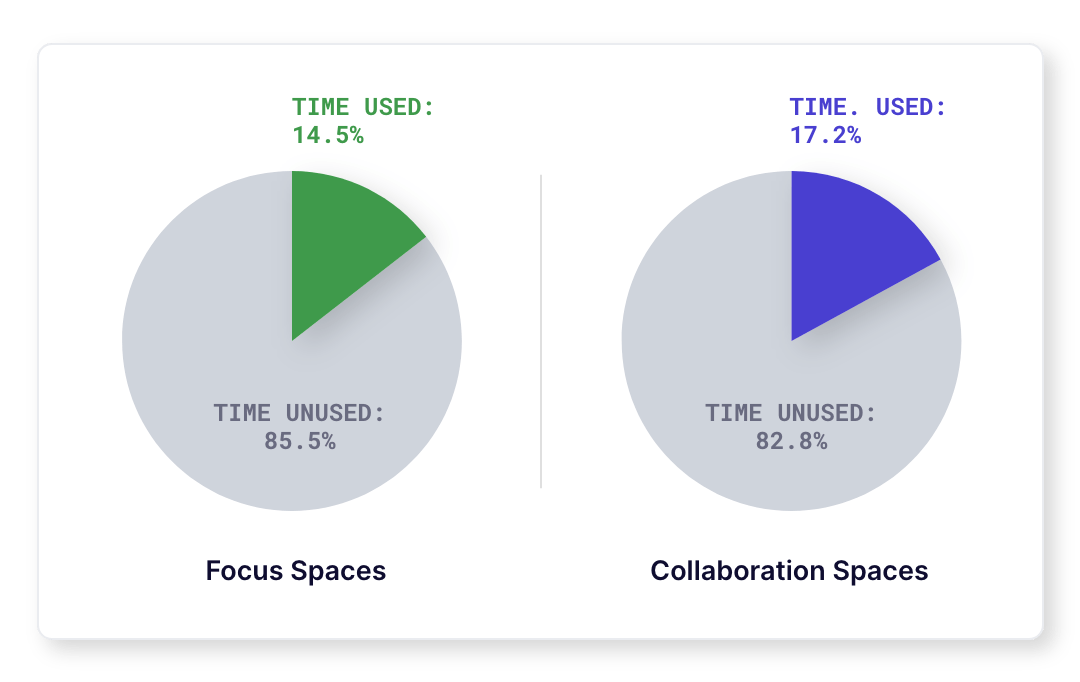

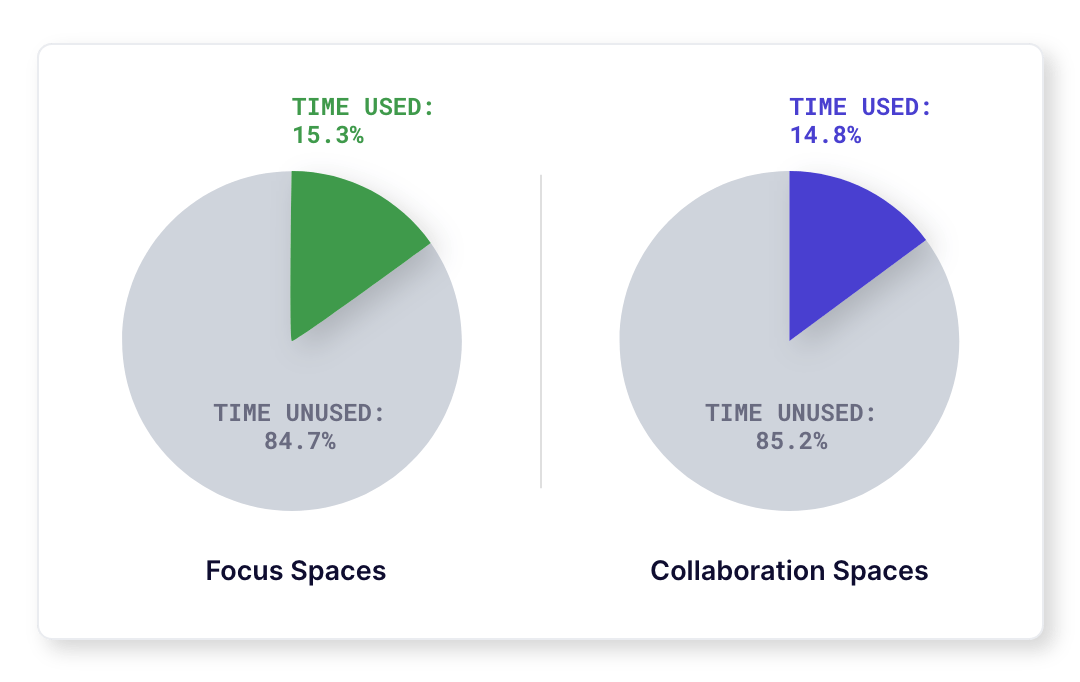

Compared to all other regions, EMEA is spending the most time in collaboration spaces, suggesting that EMEA primarily uses in-office time to collaborate versus remotely.

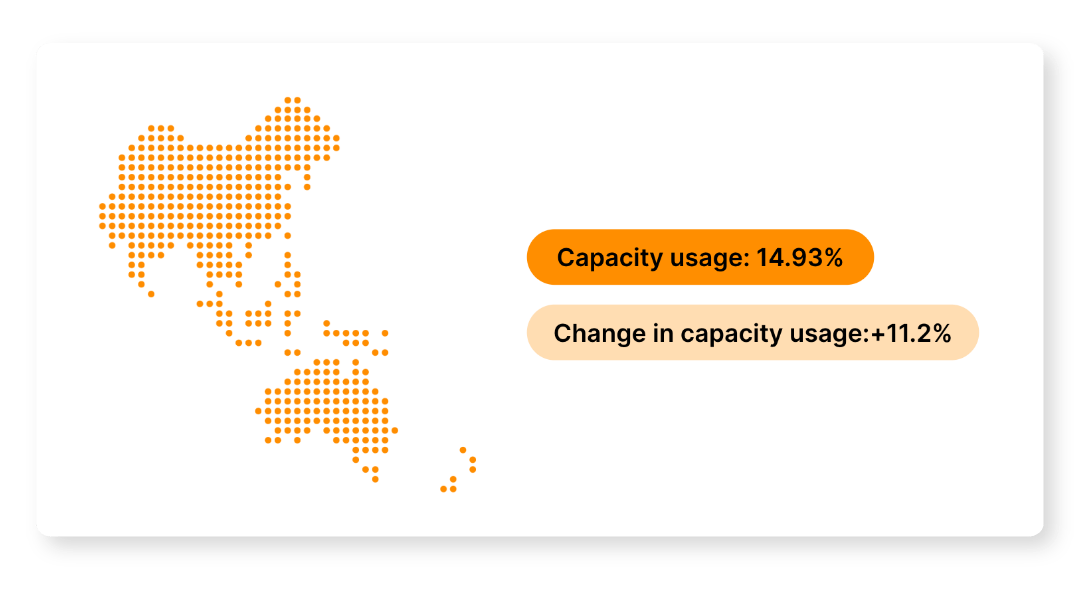

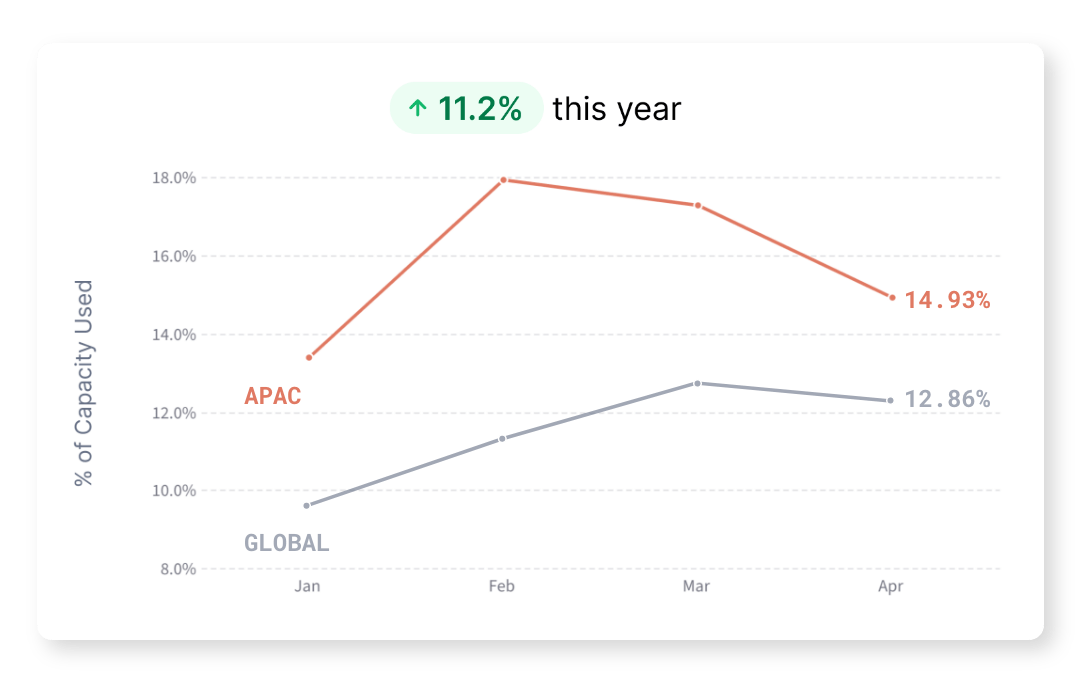

Compared to all other regions, EMEA is spending the most time in collaboration spaces, suggesting that EMEA primarily uses in-office time to collaborate versus remotely.  APAC saw notable growth between January and February, but since, capacity usage has slowly dropped, leading to overall growth of 11.2% so far this year.

APAC saw notable growth between January and February, but since, capacity usage has slowly dropped, leading to overall growth of 11.2% so far this year.  APAC has lower usage of collaborative spaces. In APAC, many meetings are held over meals, which may contribute to fewer collaborative spaces being used in-office.

APAC has lower usage of collaborative spaces. In APAC, many meetings are held over meals, which may contribute to fewer collaborative spaces being used in-office.

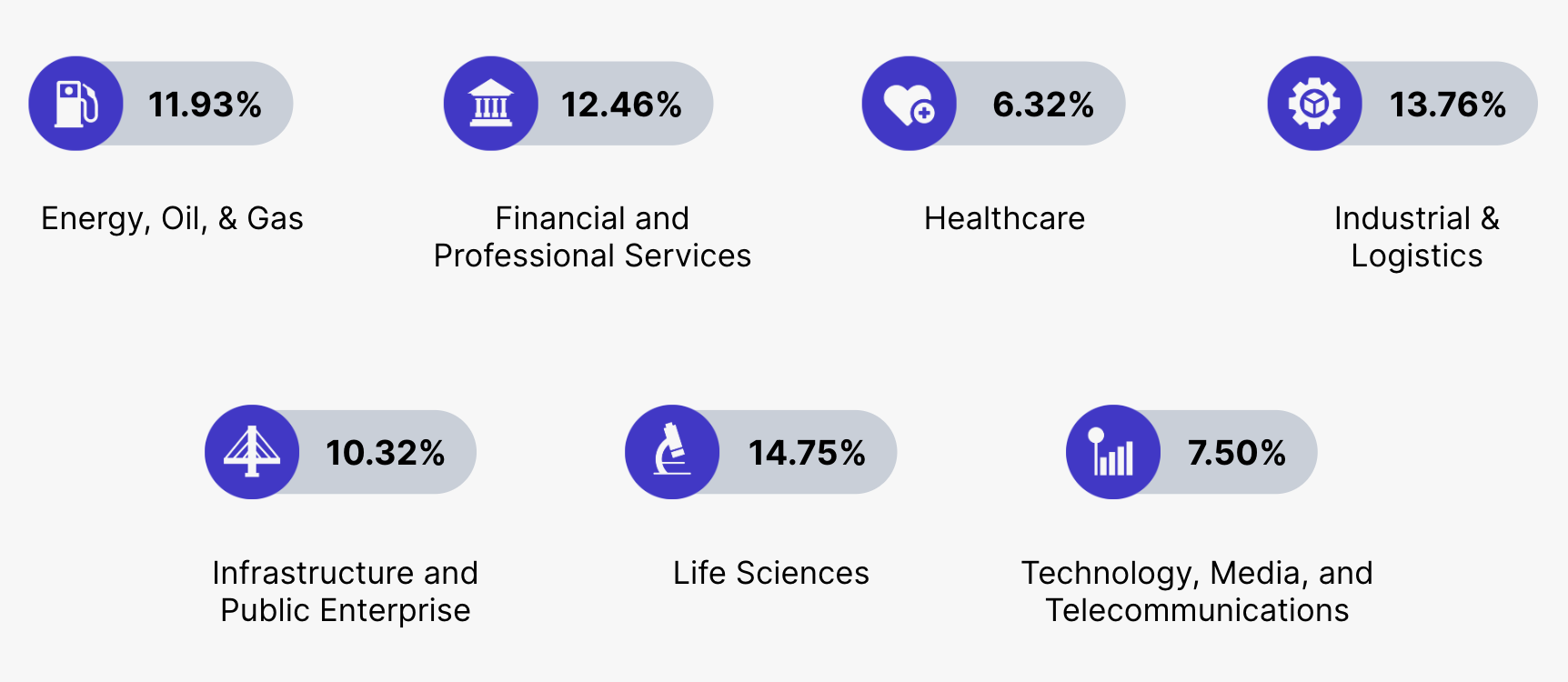

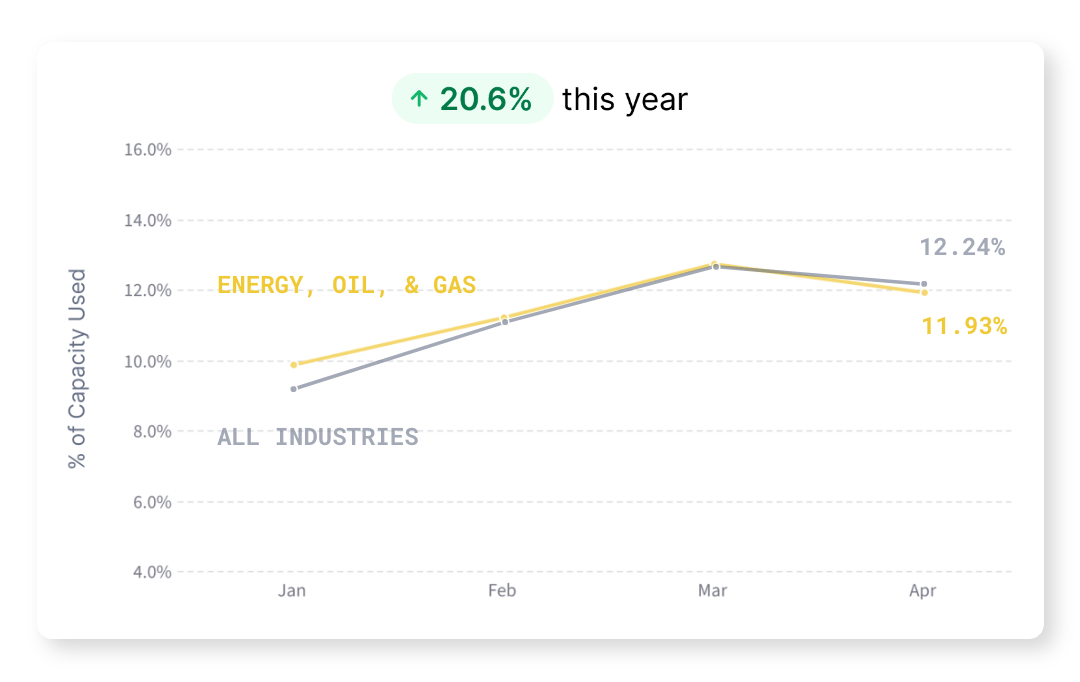

The Energy, Oil, and Gas sector is pacing closely with the global average in both capacity usage and growth. This industry also saw a small dip in usage in April, as many other industries and regions as a whole did.

The Energy, Oil, and Gas sector is pacing closely with the global average in both capacity usage and growth. This industry also saw a small dip in usage in April, as many other industries and regions as a whole did.

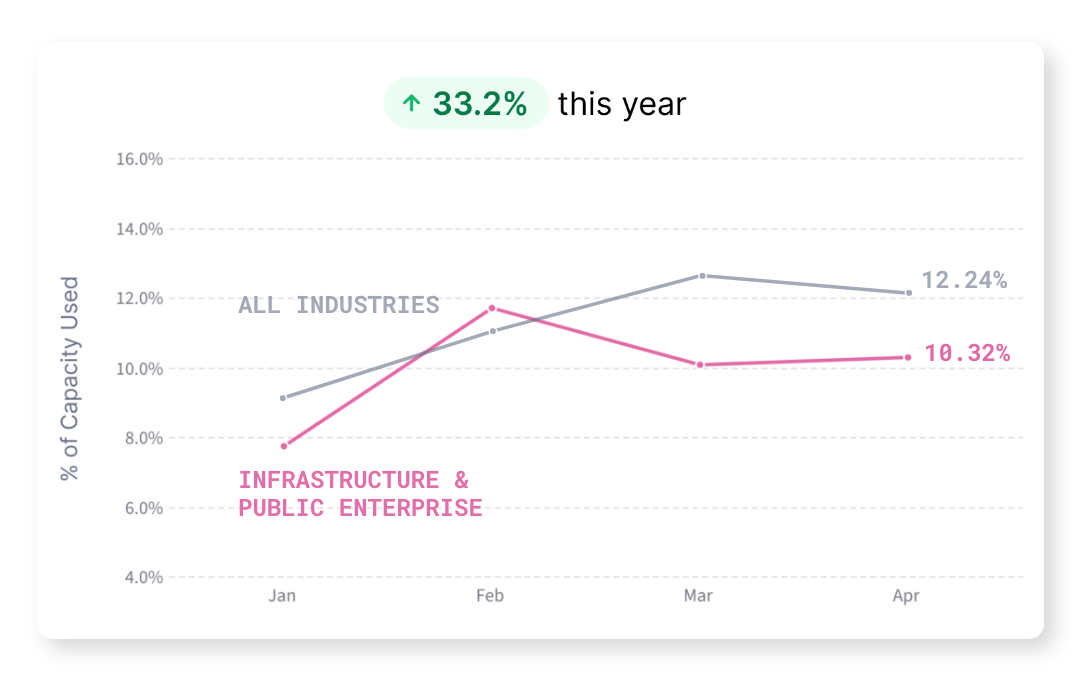

The Financial and Professional Services industry has faced significant resistance to returning to office, leading to the use of mandates, which have not been followed by everyone, as shown by slow growth.

The Financial and Professional Services industry has faced significant resistance to returning to office, leading to the use of mandates, which have not been followed by everyone, as shown by slow growth.

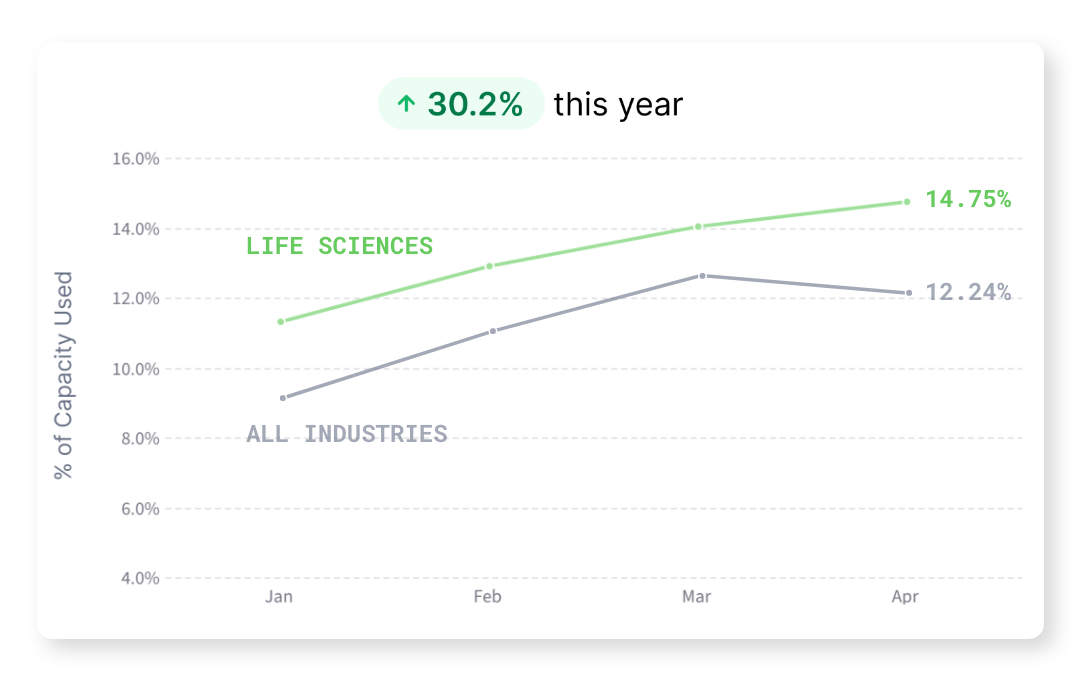

Healthcare has the lowest capacity usage among all measured industries. This low usage is due to a large prevalence of administrative and support roles in corporate healthcare that can be completed remotely. The emergence of telehealth has also created more remote and hybrid work opportunities for a historically in-person industry.

Healthcare has the lowest capacity usage among all measured industries. This low usage is due to a large prevalence of administrative and support roles in corporate healthcare that can be completed remotely. The emergence of telehealth has also created more remote and hybrid work opportunities for a historically in-person industry.

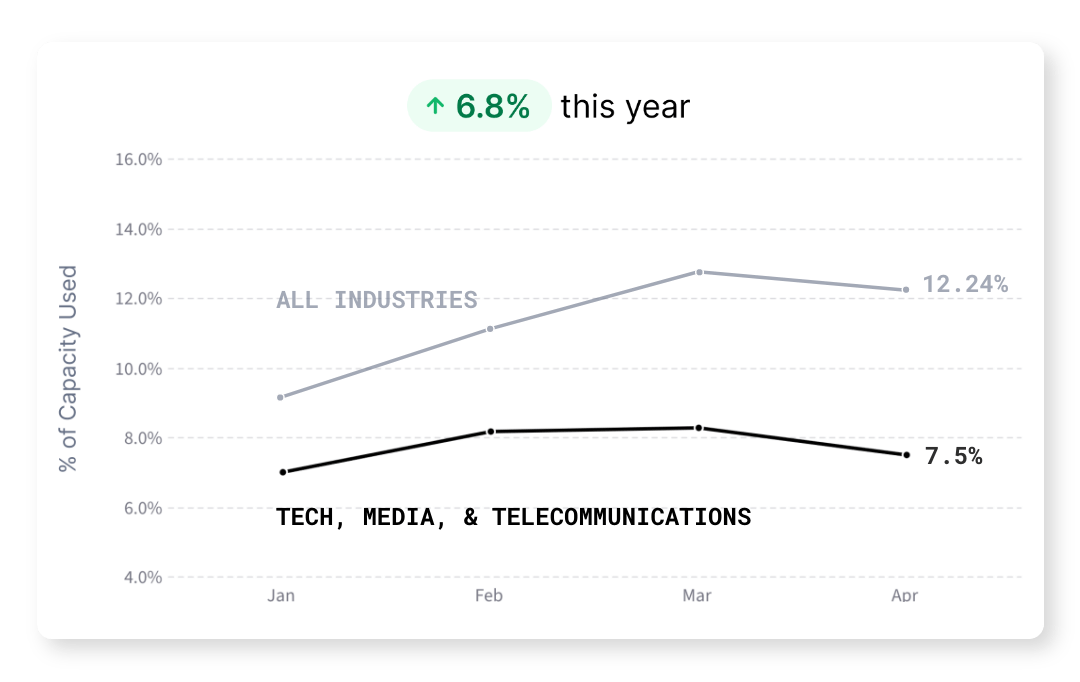

The technology, media, and telecommunications industry has the lowest capacity usage, as their focus on non-physical products (like software) enables remote work. The digital presence of their products has led to more flexible work environments and slow industry growth.

The technology, media, and telecommunications industry has the lowest capacity usage, as their focus on non-physical products (like software) enables remote work. The digital presence of their products has led to more flexible work environments and slow industry growth.